Dealing with an IRCC “Debt to the Crown”: Uncovering Fraudulent Chargebacks and How GCMS Notes Can Help

Applying for a Canadian visa or permit can be a stressful process, and having your application refused due to an IRCC debt to the Crown can cause immediate panic. If you are facing this situation, you are not alone — and you are not necessarily at fault. In this article, we explain what an IRCC debt to the Crown means, how fraudulent chargeback scams create it, why you might be completely in the dark about it, and how to uncover the truth and resolve it.

What Is a “Debt to the Crown” and How Does the Chargeback Scam Work?

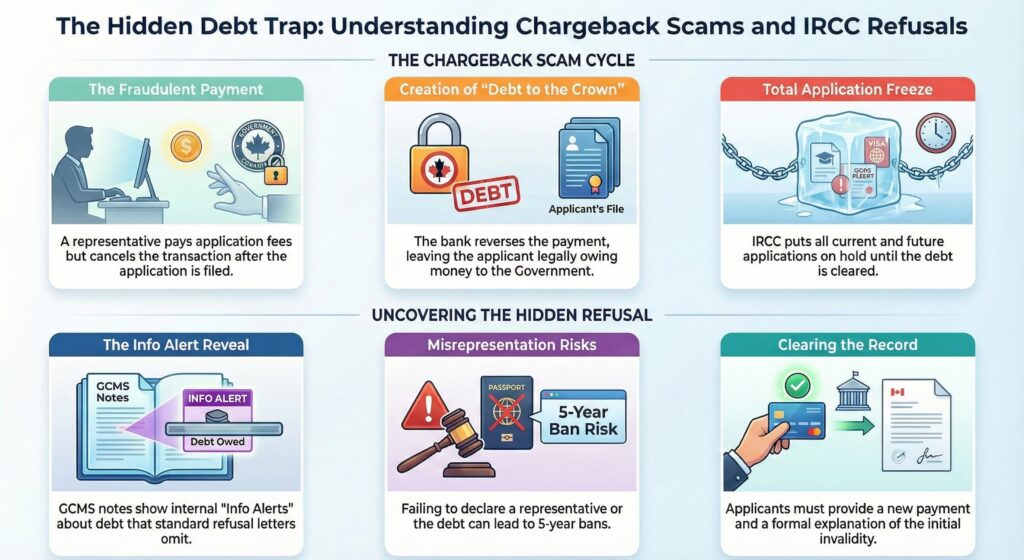

A “Debt to the Crown” simply means that you owe money to the Canadian government. While this can arise for various reasons, one of the most common causes for immigration applicants is a chargeback on the fees paid during a visa or permit application.

This typically happens through what is known as a chargeback scam involving third parties or undeclared representatives. Here is how the trap works: a credit card payment is made to IRCC during the application process, and then reversed — either by a fraudulent representative acting without your knowledge or, in some cases, by the applicant themselves under false pretenses. IRCC treats this payment reversal as fraud, and the amount owed immediately becomes a debt registered against your immigration file.

How Does a Debt to the Crown Affect Your Application?

You might assume an unpaid fee triggers an automatic system-wide freeze on your file, but that is not quite how it works. In practice, how IRCC responds falls under case-by-case officer discretion. Depending on the officer reviewing your file, the consequences can include your application being cancelled, delayed, or outright refused. An officer may also place a formal hold on your current and any future applications until the outstanding debt is resolved.

Ignoring the issue carries serious legal risks on two separate fronts:

Misrepresentation under IRPA s.40(1): Officers may raise formal admissibility concerns because of the undeclared debt and the missing payment. A finding of misrepresentation is a grave outcome and carries its own consequences.

Undeclared representative: If you used a third-party representative who was never declared to IRCC, officers may require a separate explanation for that as well. Although these two issues — the unpaid debt and the undeclared representative — are legally distinct, IRCC may raise them together and expect you to address both simultaneously.

Your Legal Culpability and the Representative Blind Spot

If you were victimized by a chargeback scam through an undeclared agent, you may be completely unaware it ever happened. All correspondence regarding the cancelled payment and the resulting debt may have been directed to the representative who submitted your file — not to you.

However, not knowing about the fraud does not automatically protect you from its consequences. Under Canadian immigration law, you are responsible for all the information contained in your application, even if a representative completed it on your behalf. If your representative commits chargeback fraud, IRCC still treats it as fraud on your file, and you could potentially be found inadmissible and banned from Canada for up to five years under IRPA s.40(2).

That said, being a victim of representative fraud is a recognized mitigating factor that immigration officers are expected to consider when assessing your case. The key is to document the fraud as clearly and thoroughly as possible — gather any evidence you have of your dealings with the representative, communications, receipts, and anything else that demonstrates you were deceived. A well-documented response gives you the strongest possible position when addressing IRCC.

The Power of GCMS Notes

If you are facing a confusing refusal and suspect a hidden issue on your file, ordering your GCMS notes is an essential first step. The Global Case Management System (GCMS) contains the exact remarks, alerts, and refusal grounds entered by the immigration officer who reviewed your application. If a Debt to the Crown is the reason your file is stalled or refused, it will be explicitly documented in these notes.

For example, when an application is refused due to an unpaid fee, the officer will typically place a specific Info Alert in the GCMS notes that reads something like this:

“Info Alert indicates that the PA has an unpaid debt to the Crown. PA has been advised to finalize payment before submitting a new application. Application refused.”

This level of detail is rarely communicated in standard refusal letters, which is why many applicants spend months confused about what went wrong. Your GCMS notes cut through that confusion and tell you exactly what is on your file, so you can take the correct corrective action rather than guessing.

How to Resolve Your Debt to the Crown

Once you have confirmed the issue — whether through your GCMS notes or a direct notice from IRCC — you need to act quickly. Here are the steps to resolve it:

Step 1 — Replace the Payment You will need to pay the outstanding fee using your own payment method. In many cases, IRCC will require you to register as a new client to submit the replacement payment. When doing so, always use a credit card or payment method held in your own name. Do not allow any third party to make this payment on your behalf.

Step 2 — Provide a Detailed Written Explanation IRCC may require a formal written explanation detailing exactly why the original payment was reversed. If the chargeback was the result of representative fraud, explain this clearly and provide all supporting evidence you have. If you also had an undeclared representative, you will need to address that separately in the same submission.

Step 3 — Submit Your Proof Provide IRCC with a copy of your new payment receipt along with your written explanation and supporting documentation. Keep copies of everything you send.

Protecting Yourself from Immigration Fraud

The best way to avoid a Debt to the Crown situation is to take precautions before it happens. Here is how to protect yourself:

Verify your representative before hiring them. Always check that any immigration consultant is registered and in good standing on the College of Immigration and Citizenship Consultants (CICC) public register at college-ic.ca. Using an unregistered or unauthorized representative is both a legal risk and a common gateway to fraud.

Always pay IRCC fees yourself. Never allow a third party — including your representative — to pay your application fees using their own credit card or bank account. Always pay directly through your own IRCC account using your own payment method. If a representative insists on handling payment themselves, treat it as a serious red flag and walk away.

Stay informed about your file. Do not rely solely on your representative for updates. You can and should monitor the status of your own application directly through your IRCC account or by submitting requests for your GCMS notes if something feels off.

Final Thoughts

A Debt to the Crown on your IRCC file can feel overwhelming, especially if you had no idea it existed. But the situation is resolvable — and if you were the victim of representative fraud, the law does recognize that context matters. The most important thing you can do is move quickly: order your GCMS notes, document everything, replace the payment, and address IRCC’s concerns in writing with as much supporting evidence as possible.

If you’ve been refused and suspect a hidden issue like a Debt to the Crown, order your GCMS notes today to get the clarity you need to move forward.